When To Take Social Security

A Social Security snapshot

Basically Social Security is a federal insurance program that provides financial support for workers who have paid into the system through FICA (Federal Insurance Contributions Act) taxes taken from their paychecks. Social Security puts the money from those contributions into one huge bucket, then pays out benefits to retirees, their families, surviving spouses, or disabled people who are eligible. In a way, it’s like the SSA takes some of your money while you work, then gives it back when you retire.

It’s a safety net, not a cash cow

The concept of Social Security is to replace some of your income based on your lifetime earnings. It was never meant to be your sole source of retirement income. In fact, benefits are meant to replace only about 40% of your pre-retirement income. Since experts advise having 70-80% on hand to live comfortably, you still need additional income streams to fill that 30% gap.

Starting early earns you less

Your Social Security benefits depend on two things: how much money you earned over your working life, and at what age you start collecting benefits. If you start at the earliest eligibility age of 62, you will receive the minimum benefit you’re entitled to. But if you wait until your full retirement age (FRA), you will receive maximum benefits. You can of course continue to work but your benefits cease growing when you reach age 70.

| If you start getting benefits at age* | And you are the: Wage Earner, the Retirement Benefit you will receive is reduced to | And you are the: Spouse, the Retirement Benefit you will receive is reduced to |

|---|---|---|

| 62 | 70.00% | 32.50% |

| 62+1 month | 70.4 | 32.7 |

| 62+2 months | 70.8 | 32.9 |

| 62+3 months | 71.3 | 33.1 |

| 62+4 months | 71.7 | 33.3 |

| 62+5 months | 72.1 | 33.5 |

| 62+6 months | 72.5 | 33.8 |

| 62+7 months | 72.9 | 34 |

| 62+8 months | 73.3 | 34.2 |

| 62+9 months | 73.8 | 34.4 |

| 62+10 months | 74.2 | 34.6 |

| 62+11 months | 74.6 | 34.8 |

| 63 | 75 | 35 |

| 63+1 month | 75.4 | 35.2 |

| 63+2 months | 75.8 | 35.4 |

| 63+3 months | 76.3 | 35.6 |

| 63+4 months | 76.7 | 35.8 |

| 63+5 months | 77.1 | 36 |

| 63+6 months | 77.5 | 36.3 |

| 63+7 months | 77.9 | 36.5 |

| 63+8 months | 78.3 | 36.7 |

| 63+9 months | 78.8 | 36.9 |

| 63+10 months | 79.2 | 37.1 |

| 63+11 months | 79.6 | 37.3 |

| 64 | 80 | 37.5 |

| 64+1 month | 80.6 | 37.8 |

| 64+2 months | 81.1 | 38.2 |

| 64+3 months | 81.7 | 38.5 |

| 64+4 months | 82.2 | 38.9 |

| 64+5 months | 82.8 | 39.2 |

| 64+6 months | 83.3 | 39.6 |

| 64+7 months | 83.9 | 39.9 |

| 64+8 months | 84.4 | 40.3 |

| 64+9 months | 85 | 40.6 |

| 64+10 months | 85.6 | 41 |

| 64+11 months | 86.1 | 41.3 |

| 65 | 86.7 | 41.7 |

| 65+1 month | 87.2 | 42 |

| 65+2 months | 87.8 | 42.4 |

| 65+3 months | 88.3 | 42.7 |

| 65+4 months | 88.9 | 43.1 |

| 65+5 months | 89.4 | 43.4 |

| 65+6 months | 90 | 43.8 |

| 65+7 months | 90.6 | 44.1 |

| 65+8 months | 91.1 | 44.4 |

| 65+9 months | 91.7 | 44.8 |

| 65+10 months | 92.2 | 45.1 |

| 65+11 months | 92.8 | 45.5 |

| 66 | 93.3 | 45.8 |

| 66+1 month | 93.9 | 46.2 |

| 66+2 months | 94.4 | 46.5 |

| 66+3 months | 95 | 46.9 |

| 66+4 months | 95.6 | 47.2 |

| 66+5 months | 96.1 | 47.6 |

| 66+6 months | 96.7 | 47.9 |

| 66+7 months | 97.2 | 48.3 |

| 66+8 months | 97.8 | 48.6 |

| 66+9 months | 98.3 | 49 |

| 66+10 months | 98.9 | 49.3 |

| 66+11 months | 99.4 | 49.7 |

| 67 | 100 | 50 |

Putting it off puts more in your pocket

Most financial experts advise delaying retirement, because your Social Security benefits continue to increase for each year you put off claiming them. This translates into a greater income stream when you finally do stop working. How long must you wait to maximize your Social Security benefits?

| If you were born in: | Your full retirement age is: |

|---|---|

| 1950 or earlier | You’ve already hit full retirement age |

| 1951-1954 or earlier | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 or later | 67 |

Source: ssa.gov.

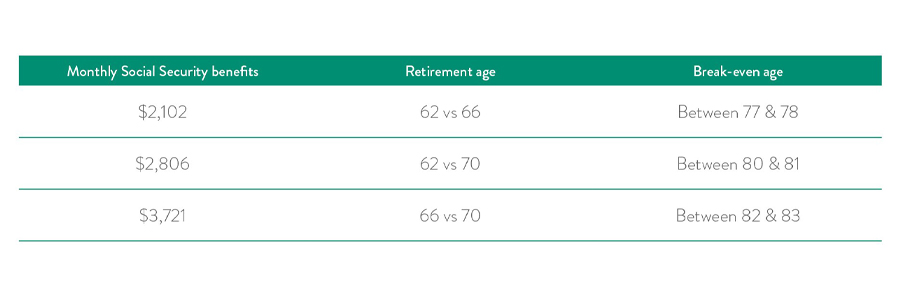

What is the break-even point?

If you wait to take Social Security until age 66 instead of at 62, you will come out ahead at age 77 or 78. The longer you wait to collect benefits, the longer you wait to break even.

Use the SSA calculator to determine your break-even age.

Early start can still be a smart way to go

For people with an average life expectancy (84 for men, and 86 for women), it almost shouldn’t matter when you start Social Security benefits. If longevity runs in your family, waiting might work best for you. But if it doesn’t, or if you are not in good health, you may want to start sooner rather than later. Here are some other reasons to consider early retirement:

- You aren’t working anymore and simply need the benefit in order to make ends meet.

- You are earning less than your spouse, who can wait to file for a higher benefit.

- You want to enable family members to receive benefits based on your work history. A qualified spouse or child could receive a payment up to half your FRA.

- You have other retirement income streams, and want to invest your benefit money. (Experts advise that with inflation, you will need an 8% annualized return to come out ahead of Social Security inflation-adjusted income.

Will Social Security even be here when you retire?

Remember that bucket of FICA money the SSA collects from every American worker’s paycheck? The latest SSA report states that bucket is going dry, and the funds will probably be completely gone by 2037. The good news is, ongoing taxes should be enough for the SSA to pay out about 76% of benefits. But its future may still be in question. So if you are eligible you may want to claim benefits while you can. If you’re far from retirement age, you should be saving hard, investing wisely and considering that any Social Security benefit you may receive will be a bonus.

What’s right for you?

Deciding when to begin taking Social Security is a very personal decision that is impacted by your financial picture, family circumstances, and often, your best guess at what the future holds for you. Rather than choosing between early retirement vs full retirement age, you should focus on finding the ‘financially optimal’ age to claim your benefits, and enjoy your retirement.