Life Insurance For Seniors:

Yes Or No?

It’s not too late

Many older Americans still have dependent spouses, mortgages, kids and grandchildren. And most of us are probably concerned about the financial situation we will be leaving behind once we pass away. Life insurance can be a viable option, depending on your circumstances and goals.

The good news is there are many programs available for older buyers, up to 80-years, and a few limited-coverage policies for people over 90. The not-so-good news is the costs increase as people age, sometimes becoming unaffordable. And once you pass the age of 70 it becomes far more difficult to be approved. So should you decide life insurance is right for you, the sooner you buy a policy, the better. Here are some tips to help you determine whether to consider buying insurance.

Do you really need it?

Take a realistic look at your financial situation. Do you have enough assets to cover all your obligations after you die? If you are not leaving loved ones with financial burdens, you may not need life insurance. Still, you may want it, for reasons such as these:

- To provide financial security for your spouse and/or dependents who may not otherwise be able to pay living costs on their own

- To enable you to leave money gifts to family members and other beneficiaries. Added bonus: a life insurance death benefit is not considered taxable income

- To pay off debt or other large financial obligations

- To cover your funeral costs

Consider your life expectancy

According to the Social Security Administration, a 65-year old man can expect to live to age 84; a 65-year old woman on average will live to 86.5. And one of every three 65-year olds will reach age 90. So it is possible you could outlive a term insurance policy, meaning after many years of paying premiums, you and your heirs would get no payoff. To avoid this problem, you’d need a more expensive permanent policy that doesn’t age out. So be sure you weigh these costs against the benefits in your decision.

On the other hand, certain insurance policies accumulate cash value that you can borrow against to help with current expenses. Some policies also earn dividends, which accrue interest that can be paid to you, or accumulated to become a higher payout.

Calculate your coverage

A life insurance policy’s coverage amount is the sum of money your beneficiaries will receive when you pass away. Many financial experts advise using this formula to determine your target coverage amount: (total financial obligations X the number of years you want to replace income) – (total liquid assets).

Your financial obligations include:

- Mortgage or rent payments

- Credit card debt

- Property taxes

- Outstanding loans

- Supplemental medical coverage

- Funeral costs

- Estimated years of lost income (such as a pension) that would need to be replaced

- Cash for an emergency fund

Your liquid assets include:

- Cash such as savings and certificates of deposit

- Bills that are receivable

- Tax refunds

- Stocks and bonds

Using the formula, if your total financial obligation is $250,000, and your liquid assets total $125,000, your ideal coverage amount would be $125,000.

Another popular way to determine the death benefit of a policy is to calculate your annual income, then multiply it by 10. That’s the payout your heirs should receive.

Most insurance companies offer a life insurance calculator to better help you determine what coverage is appropriate for your circumstances.

Types of life insurance

Here is a quick pro/con overview of the main kinds of coverage that most seniors will encounter:

Term Life Insurance

• Generally the most affordable

• You can choose the length of the policy term up to 30 years

• No medical exam required for simplified plans

• You may outlive your policy

• Renewals may be available but premiums will increase, even if your health has not changed

Whole Life Insurance

• Higher but stable premiums

• Death benefit extends for policyholder’s lifetime

• Provides great security and safety

• Accumulates cash value

• After enough time, your policy’s cash value may be used to borrow against

• Accumulated cash value is not passed along to beneficiaries

• Four types of policies are available: traditional, universal, variable and variable-universal

Guaranteed Universal Life Insurance

• Lower premium amounts than whole life insurance

• Guaranteed cash value

• Greater flexibility

• Coverage can be customized

• Guaranteed universal life insurance can provide a lifelong death benefit

• Guaranteed universal life insurance does not build cash value

• Indexed universal life insurance builds cash value based on a stock market index that increases benefit to heirs

Guaranteed-acceptance Life Insurance

• No health qualifications

• Geared toward the elderly

• Can’t be turned down as long as you are within the age requirement (usually up to 75)

• Higher premiums

• Lower payouts and death benefits

Final Expense Insurance

• Low cost

• Easy to qualify

• Funds are used specifically for burial and related expenses

• May build cash value

• Relatively low maximum death benefits, in many cases only up to $40,000

Which type is best for you?

Many insurance pros would recommend term life over whole life for seniors. That is due to the significantly higher cost of whole life premiums, and the possibility that the cash-value aspect frequently does not benefit older policy purchasers. On the other hand, a whole life policy might be a good choice if you are wealthy, not too old, and want the assurance that you will be covered for the rest of your life. If you aren’t wealthy, but still demand lifetime coverage, guaranteed life insurance might be your best option.

Here are some things to consider while you look into the various types of policies:

- Age – you have fewer options the older you are, and they all become less affordable with time. The same policy, issued to a 70-year old, could cost as much as three times the amount of the same coverage issued to a 50-year old.

- Health – the cost of your premium will also rise if you have certain medical conditions and/or risky habits, such as smoking, alcohol abuse, or dangerous hobbies like skydiving.

- Cost – if you aren’t sure you can make each monthly premium payment on time, you may lose your coverage. Many insurance companies offer a grace period for late payments.

- Limits – some policies, such as term life, may only cover you to age 80 or 85. Also, be sure to ask about any exclusions to coverage, such as death by suicide, smoking (if you claimed you were a non-smoker), criminal actions, war, and high-risk activities.

- Scams – in insurance, as in all money-making industries, marketing may not be your friend. Stay skeptical of promised amazing rates, easy approvals, or high-pressure policy pushers. And take a moment to verify your insurance agent’s license by contacting your state’s insurance commission.

Do your homework

Like all financial decisions, you must become an informed consumer, shopping for the best prices, the best benefits, and the plan that best fits your situation. Gather several quotes, based on your specific needs and circumstances. You may want to use a licensed life insurance broker who specializes in helping older adults. The broker can search multiple companies for the best options for you, rather than a company-employed agent who can only recommend programs from the insurer (s)he works for. The Society of Financial Service Professionals can help you locate a broker, here.

Look into the company issuing your coverage, because your policy is only valuable if the insurer is able to pay your heirs after you’ve passed away. Find companies with the highest credit ratings, through organizations like the Better Business Bureau, Moody’s, Standard & Poor’s. The National Association of Insurance Commissioners might be a good place to start your research.

What you could do instead

If after all your careful calculation and research you determine that life insurance is not a viable option, you can still take action to enlarge your legacy to heirs. We know there will be hefty premiums associated with a new policy. If you took that money and put it to other uses, you might be able to improve your peace of mind and beef up your estate. Here are some ways:

- Invest it to grow your wealth for heirs

- Use it to systematically pay off debts

- Arrange to automatically transfer title to your home and financial accounts to your heirs; payable-on-death (POD) accounts might be worth looking into

- Set up an emergency fund in beneficiaries’ name to they can access money faster and easier than a death benefit

Is long-term care insurance right for you?

The US Department of Health estimates that nearly 70% of today’s 65 year olds will require some type of long-term care and support in their lifetimes. Many people opt to buy a long-term care insurance policy to ensure their family doesn’t bear the financial burden for their future care needs. Medicare’s long-term care coverage is limited to skilled services or rehabilitation, for up to 100 days in a nursing home or your own home. It does not pay for custodial care or day-to-day needs.

A long-term care policy is designed to cover personal care needs, also known as activities of daily living (ADLs), including bathing, dressing, eating, incontinence/toileting, getting to and from bed, and more. Most care is provided at home, but these policies also reimburse you for care in a:

- Nursing home

- Assisted living facility

- Adult day care center

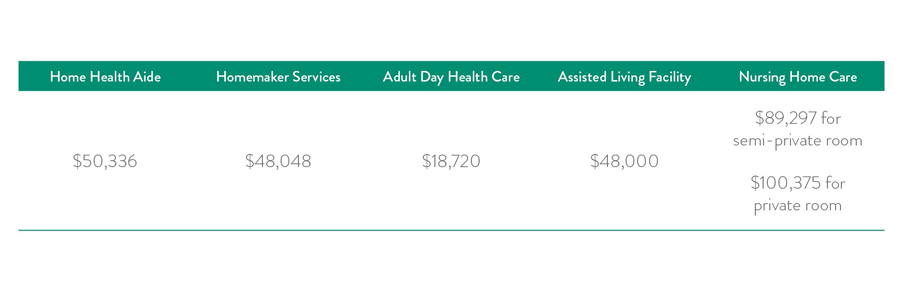

The cost of care

Many older adults will rely on their spouse or other family members for unpaid support. However, more than half of us over 65 can expect to be facing long-term health costs in future, with 15% of us racking up bills of $250,000 or more. This chart, from a recent Genworth survey, breaks down the average yearly costs:

Long-term care premium costs

For all insurance policies, the younger (and healthier) you are when you buy it, the less it costs. That’s especially true with long-term care coverage. According to recent data from AARP, the average annual premium for a 55-year old woman is about $2,600. The same coverage at age 60-year old would be $3137; at age 65, is jumps to nearly $4100. For many, the price may be beyond their means. For others, health conditions may make them ineligible for coverage at any price. And for people 70 and older, it becomes extremely difficult to find an insurer willing to give them a policy. Other factors affecting the rates you pay:

- Gender – women typically outlive men, which increases their chances of making insurance claims. Therefore, they usually pay more for a policy

- Marital status – premiums are lower for married people than single ones

- Coverage – expect to pay more for extended coverage, such as higher limits on benefits, longer number of days/years that a policy will pay, cost-of-living adjustments, and shorter elimination periods

- Insurer – the same amount of coverage can vary in price, depending on the insurance company

Premiums + time = true cost

True, long-term care premiums will cost less at a younger age. But starting later, and ultimately paying for fewer years of coverage, could add up to fewer total dollars spent, and overall lower cost to you. Let’s use the same woman as our last example, and assume she is paying premiums to age 79. If she starts her coverage at age 55, she’d pay a total of $62,100. Starting at age 60 would cost her $59,600. And if she waited to buy her policy until age 65, though her monthly premiums would be substantially higher, she’d be paying a total of $56,800, the least of the three scenarios. If you are considering purchasing a policy, ask your insurance agent to calculate your ‘sweet spot’ before making a decision.

Types of policies

You may be aware that in recent years annual premiums skyrocketed on policies sold in the 1990s and early 2000s. Insurers have fixed those problems, according to industry experts, and purchasers can expect costs to be more stable in future. Today, there are two basic types of policies:

- Long-term care insurance – these typically reimburse you for a portion of long-term care costs, for a specific period, usually between two and five years. You choose the daily or month benefit, and the coverage period, plus usually an inflation adjustment of 3% a year. Some insurers offer coverage for as long as you life, no matter what it costs, but these policies may be hard to find.

- Hybrid long-term care insurance – is now more popular than traditional coverage. With this type of policy, you are required to commit large amounts of money, such as $100,000, upfront or in installments over a certain number of years. Then any money that isn’t used for long-term care can be left to your heirs.

Bear in mind

There are fewer insurance companies offering long-term care coverage than there were 10 years ago. And the application process depends on the policy you choose. You will likely be required to have a health screening, including a physical exam, blood work, plus memory testing. If you have chronic health conditions, or are declined approval, that information goes into a database, and you will not likely find another insurer to accept you.

All long-term care policies come with an elimination period, which could mean from one to six months’ wait before your coverage kicks in.

Another consideration: long-term care insurers have been given approval to raise their premiums in recent years, which has forced many policyholders to choose between paying the higher bills, receiving reduced benefits, or canceling their coverage altogether. Some experts suggest you be prepared for premium increases of 20% every five years, and a few warn that premiums could rise 50% – 100%.

Don’t decide alone

Like any investment, the decision to buy insurance can have significant financial implications, both positive and negative. Consider your goals, do your calculations carefully, and reach out to a financial advisor, or insurance agent who specializes in elder coverage. The National Council on Aging is a good resource. Take advantage of their tools and suggestions here.